Digital Wallet: In China, Cashless is King

The popularity of digital wallet in China is celebrated. But under the veil of technological triumph, something didn’t work, some are excluded.

Written by Lok Hang Fung

Published on 06/01/2022

In August 2021, the long-awaited consumption voucher (消費券) has finally entered the digital wallets of the residents of Hong Kong. Since the announcement of the voucher initiative in late-February 2021, Hong Kongers have been complaining (Hong Kong is known as the city of complaint 投訴之都 after all) about the arrangement of the initiative – why is it all electronic? Why can’t the government just deposit the money in bank accounts like it did before? What about the elderly who have no knowledge of any kind of electronic payment? On top of these queries are suspicions of the government’s motive. Is it entirely impossible that the authority was trying to maneuver the Hong Kong population into (Chinese owned) digital payment platforms and hence pave the way for big data tracking of people’s expenses and whereabouts? Maybe yes, maybe not.

The conspiracy theory surrounding the consumption voucher initiative cannot be proven or disproven yet, but the fact that using only electronic, cashless payments to “return wealth to the people” have stirred so much controversies in Hong Kong has something to tell – that electronic payments are yet to be widely accepted in the city (especially when compared with the Chinese Mainland); that the use of electronic money would incur concerns over privacy, data leakage, theft and hacks for the people (and perhaps the risk of overspending for some),[1] and regulations and money laundering for the authorities. Still, the surge of digital wallet is unstoppable because of the hassle-free experience of paying and collecting money relatively securely. For customers, tokenisation allows transaction without disclosing their credit card information; for shopkeepers, it saves them from the tedious task of manual cash counting (remember how we hear trouble-making customers bringing tons of coins to banks or shops making news from time to time?). Perhaps even public health concerns too! Have you realised how filthy banknotes and coins can be?[2]

China: Cashless is King

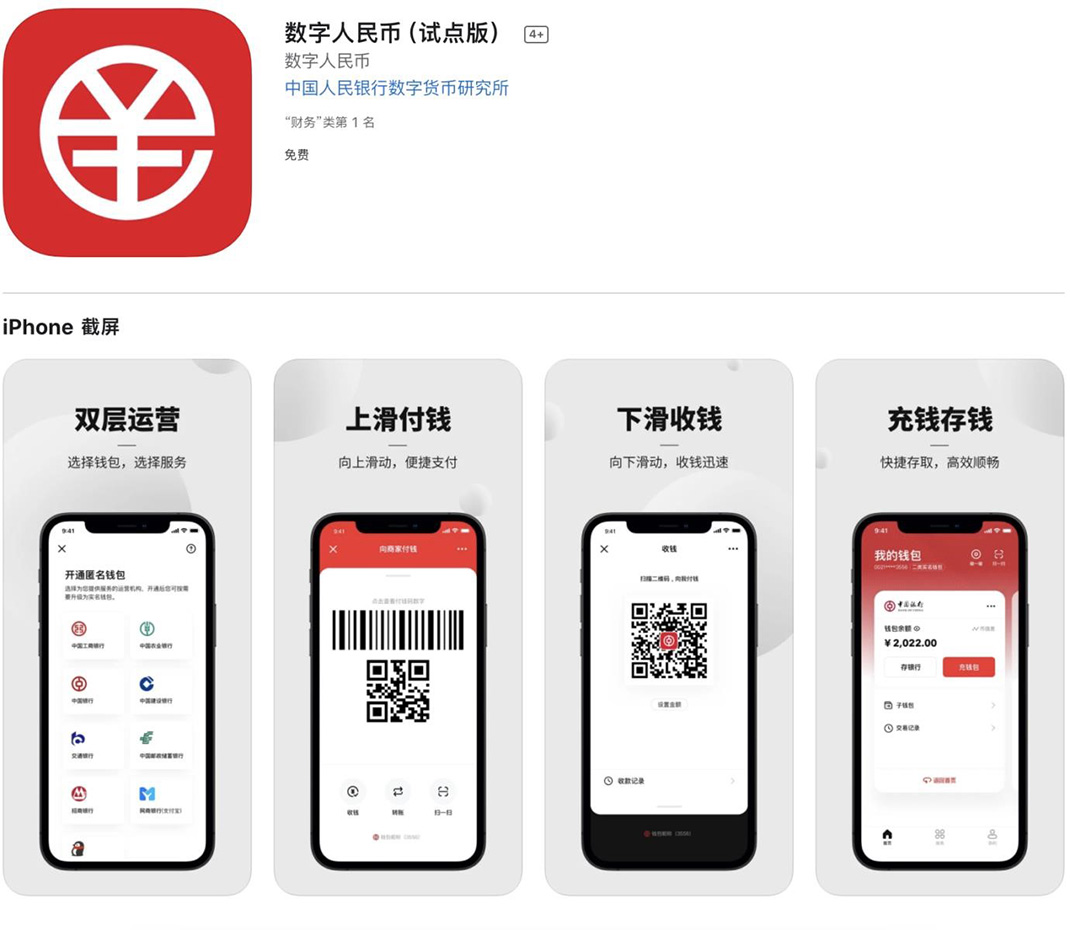

China was where banknotes were first invented and used. Ironically, it is now one of the fastest rising cashless societies in the world. While other countries go cashless with debit/ credit cards and stored value smart cards, the star in China is digital wallets including Alipay and WeChat Pay. Data in 2020 shows that a striking 72% of e-commerce spending in China is conducted using digital or mobile wallets, what is even more striking is perhaps that 50% of POS spending is also done with digital or mobile wallets.[3] It means that throughout the country of 1.4 billion population, half of the transactions at restaurants, roadside food stalls, supermarkets, wet markets, everywhere basically, are paid with QR codes and some clicks on mobile phones. China is also the first country in the world to pilot a national, state-run cryptocurrency. Highly similar to its privately-owned counterparts, the e-CNY app allows users to pay and receive money within clicks and keep track of your transaction records at ease. The only differences are that 1) you no longer draw money from your bank account to the app to reload, as the number in the app is money itself; 2) you can integrate different bank accounts all in one app and 3) the one who monitors your expenditure and how much capital you have are no longer private enterprises, but the state apparatus.

The Infrastructure

There are two prerequisites for using a digital wallet – a smartphone, and cellular network connection. China has both readily available. Most updated data to date is that 63.4% of the Chinese population uses smartphones. Part of this might have to be attributed to the growing economy of the country which allows the rising Chinese upper class and middle class to purchase smartphones, but among the over 900 million people in China who own a smartphone, a good proportion of them might be using shanzhai phones (山寨機), cheap, “copycat” mobile phones that are modelled on, but sometimes also outrun the design of more expensive, branded phones. Manufactured in Huangqiangbei (華強北) in Shenzhen, the world famous electronics manufacturing hub, shanzhai phone was once a million-dollar business (in 2010, China manufactured a total of 228 million shanzhai mobile phones).[4] Even if the shanzhai phone market is shrinking in face of a lower profit margin and fiercer competition from big brands like Apple, these cheap alternatives of fancy smartphones are still selling fast, thanks to the rise of e-commerce and the “internet celebrity economy”, especially in rural China where affording a branded phone is clearly an uneconomical choice.

If the appearance of the many shanzhai phones was market-driven, China’s cellular network coverage is more of a state project. The Chinese telecommunications industry is basically dominated by the three state-owned companies, and state policy and capital are the major advocates of the industry’s development. In 2015, the Chinese government kickstarted a pilot project to aid the poorest of villages to build 4G base stations. By 2018, 99% of the Chinese population already had access to 4G cellular networks (stability is another issue though).[5]

Do You Have a Better Option?

If you think digital wallets being so popular in China is nothing but progress, good infrastructure and a sign of advancement, you are only partly correct. For something to be so popular, there must be some other things that have not worked. In the case of China, they are physical money and credit cards. Physical money is haunted by the issue of counterfeit money. It is also not particularly easy to find an ATM in China – according to data in 2020, China has 87.88 ATMs per 100,000 adults. The number is not small (Taiwan has 157; Japan 121.71; Hong Kong 52.04),[6] but considering how big the country is, the number is not particularly impressive either. Unlike Hong Kong where you can freely withdraw money from ATMs under the same ATM network (there are two major networks – JETCO and HSBC), you need to pay a fair amount of fee for interbank ATM transactions (before the Payment & Clearing Association of China and the China Banking Association requested the lowerment of interbank ATM transaction fees to 3.5yuan per transaction in June 2021). The charge, which can be proportional to the amount of transaction, is even higher if you withdraw money in another city.

What about credit cards? Although China has an astonishing number of 0.76 billion credit cards by the end of 2020 (in other words, 0.55 card per capita),[7] credit cards have never been prominent in the country. When it was first introduced in 1985, only a few years after the Reform and Opening Up policy was in place, very few citizens could accept the idea of spending before earning. The banking system was not compatible either. Banks had no centralised credit card issue system, which made credit card applications and issues an extremely inefficient process. Also, China had its first credit scoring system (not the social one) only in 2000. Even though the number of cards issued rose year by year since the 2000s, utilisation has never been very high. Remember that China has 0.76 billion credit cards by the end of 2020? But only 14% of POS sales and 12% of e-commerce transactions were done with credit cards in the same year.[8] It is safe to say that by the time all the hardware and software were ready for credit cards to take off, digital wallets had already entered the market fiercely. If you were a small merchant or a hawker on the roadside, would you invest in a POS machine or just a QR code?

Habituating Payment

Payment is more of a habit than a choice, and the Chinese digital payment oligarchs know it well. The leading mobile payment platform in China, Alipay, started off as part of Taobao, the biggest online shopping platform in China. In other words, Alipay first existed solely for making transactions on Taobao faster, safer, and more convenient. As Taobao’s business grew massively, its internal payment system of course also came into full bloom (can you imagine having to bank in when shopping on Taobao?). But that was not the end. Alipay soon expanded its service range to every aspect of people’s lives: you can transfer money to your friends without worrying about interbank charges; you can invest in funds within clicks; you can buy things with no-interest loans (like a virtual credit card); you can even pay your electricity bill, water bills and school fees, all in one app. The expansion of digital payment’s service range shaped the payment habits of the Chinese people, who gradually found themselves more and more reliant on digital wallets, to the extent that even pickpockets have few cash to steal.

On the other hand, in Hong Kong, there is yet one platform that monopolises people’s payment in all and every aspect. Transport and small amount POS transactions are the territory of the Octopus card developed and owned by the Mass Transit Railway (MTR) Corporation. E-commerce or larger amount transactions are usually done with credit cards or bank transfer. Peer-to-peer payments in recent years have become easier with the launch of platforms that resemble functionalities of their Chinese counterparts. PayMe developed by HSBC, for example, allows P2P payments by entering recipients’ mobile numbers. More and more e-commerce merchants accept PayMe too (payment with QR code). For public service bills, PPS (繳費靈) is more often used. In a lot of cases, still, cash is king.

Source: Wikimedia Commons, commons.wikimedia.org.

Ahead of the World

Some might perceive the Chinese development of digital payment as the nation’s pride or as a proof of the nation’s advancement. It is true in some sense, but not necessarily the full picture. Digital payments have certainly provided people of all walks of life with great convenience, but at the same time excluded those who are too poor to even purchase a shanzhai phone, or whose home is too remote to be covered by 4G network. The advancement of such forms of payment also reflects the deficiencies of other modes of transactions. And while indulging in the hasslefree payment experiences within clicks on the mobile phone, one might need to also bear the risk of data leakage, and selling information about their spending habits to whoever wants them.

Footnotes

- Jacob Passy, “All the ways mobile wallets can do serious damage to your finances,” MarketWatch, 29 March, 2019, https://www.marketwatch.com/story/thisis-what-a-mobile-wallet-could-to-your-holiday-spending-its-not-pretty-2018-12-03.

- Emmanouil Angelakis et al., “Paper Money and Coins as Potential Vectors of Transmissible Disease,” Future Microbiol 9, no. 2 (2014): pp. 249-261, https://doi.org/10.2217/fmb.13.161.

- Worldpay from FIS, The 2021 Global Payments Report, https://offers.worldpayglobal.com/rs/850-JOA-856/images/1149143_GPR_DIGITAL_ALL_PAGES_SINGLES_RGB_FNL8B.pdf? mkt_tok=ODUwLUpPQS04NTYAAAF7dBt8aCWlJSdupj5JiqwBi0LqoV7CKincHYty s2oqvJMMKE0DkZ6w5Ltqgy8hjPIMe8BOBe2rqkWpiRpqTZJ_jyjdjcld0JNuQ9zDAI2 FADhyYJI.

- Fang Nan 方南, “Diaoyan jigou pao shanzhai shouji weisuo lun: 2012 nian qi fuzengzhang” 調研機構拋山寨手機萎縮論:2012年起負增長 [Polling organisation postulates the shrinkage of the shanzhai phone market: negative growth since 2012], Nanfang dushi bao 南方都市報, December 22, 2012, https://tech.qq.com/a/20101222/000063.htm.

- Liu Yuying 劉育英, “Zhongguo 4G wangluo fugai 99% renkou Chao 95% xingzhengcun tong guangxian kuandai” 中國4G網絡覆蓋99%人口 超95%行政村通光纖寬帶 [The 4G population coverage rate in China reached 99%, over 95% of villages have coverage of fibre optics broadband], Chinanews.com, June 11, 2018. https://www.chinanews.com.cn/cj/2018/06-11/8534797.shtml.

- Peng Zhengling 彭禎伶, “Zou dao na ling dao na Tai ATM mijiju quanqiu diyi” 走到哪領到哪 台ATM密集度全球第一 [Withdraw money wherever you go; Taiwan’s ATM intensity ranks first in the world], Commercial Times, January 17, 2020. https://ctee.com.tw/news/finance/208017.html.

- Qiu Haifeng 邱海峰 and Jia Runmei 賈潤梅, “Quanguo xinyongka he jiedai heyi ka zaiyong fakaliang chao 7.6 yi zhang” 全國信用卡和借貸合一卡在用發卡量超7.6億張 [Number of credit cards and quasi-credit cards issued in China passes 0.76 billion], People.cn 人民日報網上版, January 28, 2021. http://finance.people.com.cn/n1/2021/0128/c1004-32014649.html.

- Worldpay from FIS, The 2021 Global Payments Report, https://offers.worldpayglobal.com/rs/850-JOA-856/images/1149143_GPR_DIGITAL_ALL_PAGES_SINGLES_RGB_FNL8B.pdf? mkt_tok=ODUwLUpPQS04NTYAAAF7dBt8aCWlJSdupj5JiqwBi0LqoV7CKincHYty s2oqvJMMKE0DkZ6w5Ltqgy8hjPIMe8BOBe2rqkWpiRpqTZJ_jyjdjcld0JNuQ9zDAI2 FADhyYJI.